The memory chips "supercycle" is coming, will SanDisk and Micron be the next winners in the AI golden age?

RockFlow Shayne

November 18, 2025 · 16 min read

Key points:

- While everyone is fixated on computing power, a "storage crisis" is erupting. This has forced memory giants to embark on a high-stakes gamble: pouring all resources into HBM high-speed memory, which offers profits several times higher. This HBM4 arms race is about who can win orders from AI giants like NVIDIA and determines the flow of Science and Technology Wealth Center in the coming years.

- Technologies such as AI video generation are creating an unprecedented "data tsunami", making low-cost, high-density flash memory (NAND) the new favorite in data centers. The market is currently revaluing the two major storage giants, Micron and SanDisk: their fundamentals are strong and growth is accelerating, yet their share prices were previously far below the industry average. This presents investors with a rare "asymmetric" investment opportunity.

- In the past, the prices of memory chips have always fluctuated greatly with economic fluctuations and industry cycles, but the demand brought by AI is structural and exponential, and it is breaking the "cycle curse" of the memory industry. Memory is expected to grow into a high-growth, high-barrier technology track.

In the early days of the artificial intelligence wave, capital and attention were focused on the arms race of GPU computing power. However, as the scale of large AI models enters the PB era, a new bottleneck has emerged: the storage crisis. Expensive GPUs are being slowed down by inefficient storage and memory bandwidth, resulting in low computing power utilization and becoming an invisible killer of the total cost of ownership (TCO) of AI infrastructure.

Storage, an industry traditionally regarded as an "accessory," is undergoing a significant upgrade. Whether it's Model Training, Data lake archiving, or the explosive demand for capacity from future AI-generated videos, all point to a clear conclusion: storage is the real upper limit determining the scale and business efficiency of AI.

In this article, the RockFlow Investment Research Team will conduct an in-depth analysis of how AI is driving a multi-year "memory supercycle", focusing on the three core tracks of HBM (High Bandwidth Memory), DRAM, and NAND. Through in-depth analysis of leading US stock companies such as Micron (MU) and SanDisk (SNDK), we will build an investment map for the AI storage era for you.

"Computing power scarcity" has shifted to "memory scarcity"

The characteristics of AI workloads—high concurrency, large datasets, and random read/write—pose disruptive challenges to traditional storage architectures.

In AI servers, the idle time of GPUs is often due to waiting for data to be transferred from storage units to computing units. According to industry estimates, 30%-50% of the energy consumption in AI servers may be used for data movement rather than actual computation. This inefficiency directly leads to a decrease in the utilization rate of high-value GPUs and exacerbates the total cost of ownership (TCO) of AI infrastructure.

The AI era requires storage to have three key attributes: extremely high capacity (Capacity), extremely high bandwidth (Bandwidth), and low latency (Latency). This demand has propelled the storage market towards dual structural growth: the bandwidth revolution (HBM/DRAM) and the capacity explosion (NAND/SSD).

The explosive demand for HBM is reshaping the traditional DRAM market in unexpected ways. HBM consists of stacked DRAM chips, and its Average Selling Price (ASP) is significantly higher than that of traditional DDR memory.

The "siphon effect" of HBM is very pronounced. Memory manufacturers (such as Micron, SK Hynix, and Samsung) have stronger incentives to shift DRAM wafer production capacity towards manufacturing HBM base chips, which offer higher profit margins. This internal capacity shift has led to supply tightness in the traditional memory market.

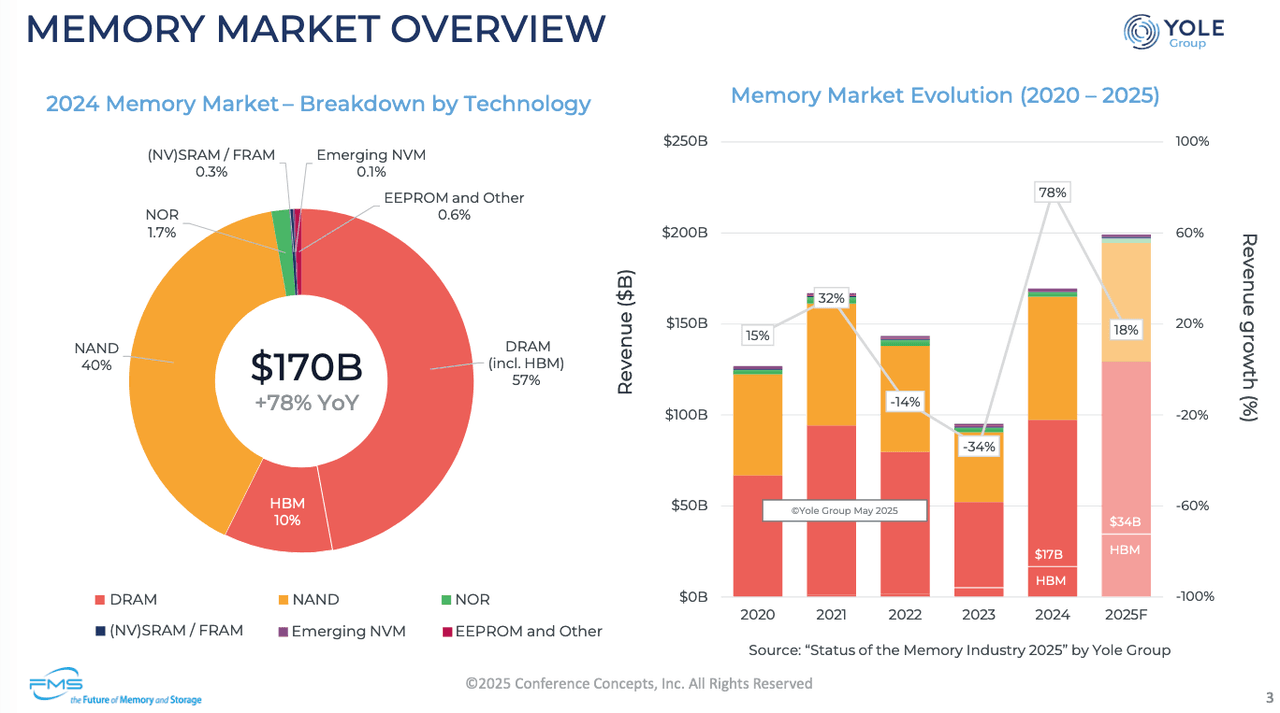

The resulting market impact is also very direct: manufacturers announced the halt of DDR4 production to make room for HBM. The rush by existing OEMs to purchase DDR4 has caused its price to skyrocket by more than fourfold in a short period. This indicates that HBM's occupation of production capacity has directly raised the cost baseline of the entire memory market. The approximately 20% increase in DRAM prices and the approximately 10% increase in NAND prices mark the beginning of a new round of the "memory supercycle".

In addition, given that the storage demand brought about by AI is non-cyclical, the commitment of large technology companies to continue increasing investment in AI infrastructure in 2026 confirms the persistence of this growth momentum. The explosive growth of AI demand far outpaces the expansion speed of traditional DRAM/NAND production, leading to a continuous imbalance between supply and demand, especially for HBM, which is expected to remain in short supply until the end of 2026.

The Arms Race of HBM4 and the Rise of QLC NAND

Competition in the memory market is shifting from capacity competition to the race for technological high ground.

The competition for dominance in HBM4 is fundamentally a challenge of advanced packaging and performance limits. HBM4 memory itself is already extremely expensive, and its price will only get higher. Establishing market dominance in HBM is crucial for memory manufacturers.

Currently, SK Hynix has been leading the HBM field. By stacking DRAM and switching the base chip to a true logic process technology such as 5nm, they have demonstrated a mass production-level speed of 10 Gbps/pin, establishing a first-mover advantage. But at the same time, Micron and Samsung are also continuously catching up: After Samsung overcame the yield issues of HBM3E, it reached a cooperation with AMD's MI350 platform. Micron reported a transmission rate of 9 Gbps/pin for its HBM4 samples, but is facing a new industry standard set by customers such as NVIDIA, which requires an upgrade to 11 Gbps/pin. Micron is shifting from self-developed memory nodes to collaborating with TSMC to develop base chips, using logic node processes such as 5nm to break through speed limits.

Therefore, this HBM4 arms race is the key to determining who will emerge victorious in this round of the memory supercycle, and its high Average Selling Price (ASP) will be the core factor determining the profitability of future memory manufacturers.

On the other hand, the revolution in high-capacity storage is also in full swing. Technologies such as AI video generation (e.g., Sora-2, Meta Vibes) have brought about explosive growth in data volume, transmitting storage demand from DRAM to NAND flash memory.

Traditional data is stored in nearline Hard Disk Drives (HDDs). However, the surge in AI data volume has led to HDDs facing supply chain shortages, with delivery cycles as long as one year and prices skyrocketing. Enterprise Solid State Drives (eSSDs), with their higher density, lower power consumption (about 30% reduction), and faster access speed, are accelerating the replacement of HDDs.

There is also the rise of QLC NAND - Quad-Level Cell (QLC) NAND flash memory has become an ideal choice for AI hyperscale data centers due to its lower cost and higher storage density.

For example, SanDisk recently released the UltraQLC SSD, with a single drive capacity of up to 256TB, far exceeding the current maximum capacity of HDDs, and is highly suitable for AI video and data processing. The storage density and energy-saving advantages of QLC make it an inevitable mainstream choice for cloud service providers.

CXL technology is emerging as the third key catalyst in the AI storage ecosystem. CXL allows CPUs and GPUs to share a memory pool, greatly enhancing the flexibility of memory capacity and bandwidth and effectively solving the memory wall problem. Type 3 CXL memory expansion devices can expand storage capacity and bandwidth without increasing the number of main CPU memory channels, reducing the total cost of ownership (TCO).

According to statistics, more than 200 companies have already joined the CXL Alliance, marking that CXL is becoming the consensus for the memory interconnect technology of processors. With the introduction of CXL 2.0/3.0 specifications, memory pooling and resource sharing will significantly improve the memory utilization of AI workloads.

In the storage sector, what are the high-quality investment targets?

Micron Technology (MU): An Undervalued AI Memory Leader with Ambitious Aspirations in the HBM Space

Micron Technology is one of the world's top three DRAM and NAND manufacturers, and the core of its investment logic lies in the explosive growth of its DRAM business (especially HBM) in the AI wave, as well as its relatively undervalued stock price.

RockFlow's investment research team believes that Micron's growth story is transcending traditional cyclical fluctuations and evolving into a structural expansion. Its solid fundamentals have the following three major highlights:

Stunning Growth in DRAM Revenue: Micron's DRAM business revenue in the fourth quarter of fiscal year 2025 increased by nearly 69% year-on-year, significantly accelerating compared to the growth rates of the previous two quarters. This growth rate far exceeded the semiconductor industry's average growth rate of 25% during the same period, demonstrating that Micron is effectively leveraging the structural opportunities brought by AI. Wall Street analysts expect that Micron's average annual growth rate in the next four quarters will remain above 40%. Innovation-driven and R&D investment: Micron continues to increase its R&D investment, with R&D spending in the past 12 months approaching a new high of nearly $4 billion. This is not a cost burden but a strategic investment for it to maintain its leading position in the industry. AI Data Center Solution: The newly launched ultra-high-capacity SOCAMM2 LPDRAM is specifically designed for AI data centers, meeting the LLM's demand for ultra-high-capacity and high-energy-efficiency memory. High-performance gaming memory: The simultaneous launch of the most powerful gaming memory, DDR5 Pro OC 6400 CL32, demonstrates that Micron also has a clear diversified layout in the rapidly growing video game market.

Financial Health and Rigor in Capital Allocation: Despite significant investments in R&D and capital expenditures, Micron has achieved a notable reduction in net debt through rigorous capital allocation. A healthy Balance Sheet enables it to continue investing in the high-cost, high-risk HBM growth track while maintaining financial stability.

Micron's execution capabilities in the HBM field are the key to whether its future valuation can be further enhanced.

As previously mentioned, the main challenge Micron currently faces is that it has reported a transmission rate of 9 Gbps/pin for HBM4 samples, but large buyers such as NVIDIA are demanding a higher data rate of 11 Gbps/pin. Micron previously used its self-developed 1-beta memory node as the base chip for HBM, which has a lower cost but limits its ability to achieve higher data rates.

To overcome the speed bottleneck and ensure market competitiveness, Micron announced a partnership with TSMC to develop HBM4 base chips. This is a key initiative to stay ahead in the HBM4 race.

Despite Micron's strong fundamentals and remarkable growth, its forward Price-To-Earnings Ratio and Price/Free Cash Flow Ratio remain significantly below the industry median. This substantial stock price discount indicates that the market has not fully priced in the long-term structural profits brought about by HBM.

Therefore, in the view of the RockFlow Investment Research Team, Micron has the advantages of technological innovation, market leadership, and financial health, and the undervaluation of its stock price is a temporary market misalignment. Investors can regard Micron as a core investment target in the AI storage field that perfectly combines high growth, high R&D investment, and prudent capital allocation.

SanDisk (SNDK): Leader in NAND Flash Memory and Capturer of Capacity Demands in the AI Era

As a pure NAND flash company spun off from Western Digital (WDC), SanDisk (SNDK) is becoming a key beneficiary of the capacity explosion wave in the AI era, thanks to its strategic layout of enterprise SSDs (eSSDs). Its investment rationale is based on its strategic clarity, product line alignment with AI demand, and severely undervalued stock price.

SanDisk's rise is the result of its transformation from a cyclical manufacturer to a core supplier of AI infrastructure. Currently, there are four key reasons why the RockFlow Investment Research Team is bullish on it: Strategic Clarity and Profitability Priority: After the spin-off in February 2025, SanDisk clearly focused on NAND flash memory, shifting its strategic focus from "growth at all costs" to profitability. This new discipline is reflected in supporting pricing through controlling production volume and capacity utilization. Accelerated performance growth: Strategic and market improvements have directly translated into strong financial performance. SanDisk's financial reports have consistently exceeded expectations, and it has clearly indicated that price increases have begun. Its cloud end-point market grew by 195% year-on-year in fiscal year 2025, a strong testament to AI-driven demand. Product line alignment with AI requirements: "Stargate" Platform: The upcoming "Stargate" enterprise-level SSD platform, a core catalyst, features a newly designed ASIC chip and next-generation BiCS 8 QLC technology, targeting the massive, high-density storage required for AI Model Training and inference. High-capacity leader: Solid-state drives based on UltraQLC, with a single drive capacity of up to 256TB, possess significant storage density and energy-saving advantages, making them an ideal solution for AI video processing and Data lake storage. Joint Venture Advantage: A 25-year joint venture with Kioxia, sharing manufacturing and technology resources (including BiCS 8 node), has ensured SanDisk's manufacturing scale and technology roadmap.

However, it is also necessary to note some of its current risk factors: First, from the perspective of the current competition landscape: the four giants in the HBM field (SK Hynix, Samsung, Micron, and Kingston) are its formidable competitors, especially in the enterprise-level SSD market. Secondly, the vast majority of its products are not made in the US: 95% of the company's products are produced overseas, making it vulnerable to supply chain disruptions and tariffs. Third is the structural limitation: As a condition of the tax-free spin-off, SanDisk is restricted from conducting certain M&A activities within two years, which may limit its strategic flexibility in industry consolidation.

In summary, SanDisk represents a growth stock with severely undervalued value in AI storage investments. It has long-term growth opportunities in the NAND flash and enterprise-level storage markets, and is a core investment target in the AI field with strong brand value, technological innovation, and high-density storage capabilities.

High-quality investment targets in other AI storage sectors

In addition to the core memory manufacturer Micron Technology (MU) and the pure NAND leader SanDisk (SNDK), US stock investors can also capture multi-dimensional opportunities in the AI storage ecosystem through the following individual stocks and ETFs:

-

Western Digital Corporation (WDC) As the former parent company of SanDisk, it holds approximately 19.9% of SNDK's stock and indirectly enjoys its growth dividends. Meanwhile, the HDD business benefits from the shortage of nearline storage and complements eSSD. It is a channel for indirect investment in SNDK, and the HDD business still has an irreplaceable position in the explosion of AI data.

-

Intel (INTC) INTC's CPU platform (Xeon)'s demand for memory bandwidth and capacity directly drives storage upgrades. CXL, which enables memory pooling, is the key to solving the AI memory wall. It is an effective way to capture the CXL technology dividend in AI infrastructure.

-

NVIDIA (NVDA) As the largest buyer of HBM, its GPUs' consumption of HBM has increased exponentially, directly driving the entire memory supercycle. Although it is not a storage stock, its performance and product roadmap are the most direct indicators for judging the prosperity of the HBM market.

-

iShares Semiconductor ETF (SOXX) A well-known semiconductor ETF that covers chip design, manufacturing, and memory giants such as Micron, NVIDIA, and AMD, diversifies investments across the entire AI infrastructure supply chain, including storage, logic chips, and foundry segments. It is suitable for investors who wish to capture the dividends of the entire semiconductor cycle but do not want to be overly concentrated in a single storage stock.

-

VanEck Semiconductor ETF (SMH) Another well-known semiconductor ETF, complementary to SOXX, ensures that key equipment and manufacturing links in the HBM supply chain are not missed. By tracking the performance of the entire industry, it mitigates the risk of a single company losing the HBM race or facing execution risks.

Conclusion

The RockFlow investment research team believes that the "storage crisis" brought about by AI is real and long-lasting. The storage industry has entered a multi-year supercycle jointly driven by the bandwidth revolution and capacity explosion.

Currently, AI's demand for storage is exponential, weakening the cyclical nature of the storage industry and making structural growth the main theme. Driven by HBM premium and CXL innovation, storage stocks are no longer simply cyclical stocks but growth stocks in the guise of technology.

Given that the current market still has a "mismatch" between valuation and fundamentals, especially among companies such as Micron and SanDisk, investors should focus on leaders who can effectively manage capital allocation and achieve breakthroughs in the high-end storage sector. Against the backdrop of continued strong AI demand, now is the golden period to position core AI storage targets with technological advantages and attractive valuations.

Related Content